The current Uniform CPA Examination® is changing significantly in January 2024 under the CPA Evolution Initiative. It is important that you learn about this initiative and the upcoming changes to the 2024 CPA Exam to fully understand how it may impact your journey to become a CPA. Below, are frequently asked questions to help you better prepare for these changes. If you have additional questions that are not outlined below on the CPA Evolution licensure model, the 2024 Examination or the transition policy, please reach out to us at [email protected].

Q1 – Will this impact me if I am currently in the process of taking the CPA Exam?

A1 – If you successfully pass AUD, BEC, FAR and REG and retain credit for each before December 31, 2023, you do not need to test under the 2024 CPA Exam. You must simply meet the other requirements for licensure (education and experience requirements, and in many states, an ethics examination) and apply for your CPA license.

Q2 – If I haven’t passed all four parts of the current CPA Exam before January 2024, do I have to start over under the 2024 CPA Exam?

A2 – Absolutely not. The purpose of the CPA Exam transition policy is to allow you to continue your CPA Exam journey from where you are when we transition to the 2024 CPA Exam. Just follow the Transition Policy chart and see what section of the 2024 CPA Exam maps to your current passed section. Your current credit will become a credit for the 2024 CPA Exam section.

Q3 – Will my credit expiration dates for sections I have already passed change because of the transition?

A3 – No. Even though you now are getting credit for a new section because of the transition mapping, your credit expiration date will remain the same as it was for the Exam section you previously passed (see Q8/A8 below for possible extension dates on sections passed at 1/1/24).

Q4 – Will I be able to take all current CPA Exam sections through December 31, 2023?

A4 – No. It is currently anticipated that the final day for testing of all current CPA Exam sections (AUD, BEC, FAR and REG) will be December 15, 2023. No CPA Exam sections may be scheduled from December 16, 2023, through January 9, 2024, to allow for conversion of IT systems to the 2024 CPA Exam sections. Candidates are encouraged to plan their testing schedules accordingly.

Q5 – Will I be able to take AUD, FAR and REG multiple times late in 2023?

A5 – While there will be no cutoff for initial or reexam applications for AUD, FAR and REG, like that for BEC, candidates are reminded that the final date of testing for all current CPA Exam sections will be December 15, 2023.

Q6 – Will I be able to take BEC multiple times late in 2023?

A6 – Candidates need to be aware that there will be a cutoff for applications (both initial and reexam) for BEC in Fall 2023. Each individual Board of Accountancy must determine the application cutoff date for candidates in its jurisdiction. NASBA will publish these dates on its website as those dates are established. Candidates should not anticipate having the ability to test BEC multiple times in November and December 2023. We encourage candidates to plan accordingly. It is anticipated that many candidates will be testing late in 2023 and appointments for testing will be highly utilized.

Q7 – What if I don’t complete BEC in 2023? Will I be able to take BEC in 2024?

A7 – No. The final date for taking the BEC section is December 15, 2023. BEC will not be available after that date nor in 2024 or beyond. Please review the Transition Policy Chart to better understand which sections can be taken in lieu of BEC in 2024, if necessary.

Q8 – I understand there is a credit extension policy that adds time to the credit period for any credits that I might have outstanding on January 1, 2024? How can I find more information about that policy?

A8 – It is very important to know if this policy applies to you. Boards of Accountancy must each determine if this policy will apply to candidates in their jurisdictions. Please refer to this map to know the status of the policy adoption in the jurisdiction to which you applied. Several Boards of Accountancy will be taking up consideration of this policy at meetings yet in 2022 and early 2023, so please refer back to the map on NASBA’s web site for updates.

Q9 – When will I be able to apply to take one of the 2024 CPA Exam sections?

A9 –Each Board of Accountancy will determine when candidates can start submitting applications for the new Discipline sections. The specific dates are yet to be determined but will be posted when available. Notices to Schedule for AUD, FAR and REG may be used to schedule current Exam sections in 2023, as well as the new core sections in 2024, so there will be no change to the application process for those sections. The AUD, FAR or REG Exam section taken is based on whether the candidate schedules to test in 2023 or 2024.

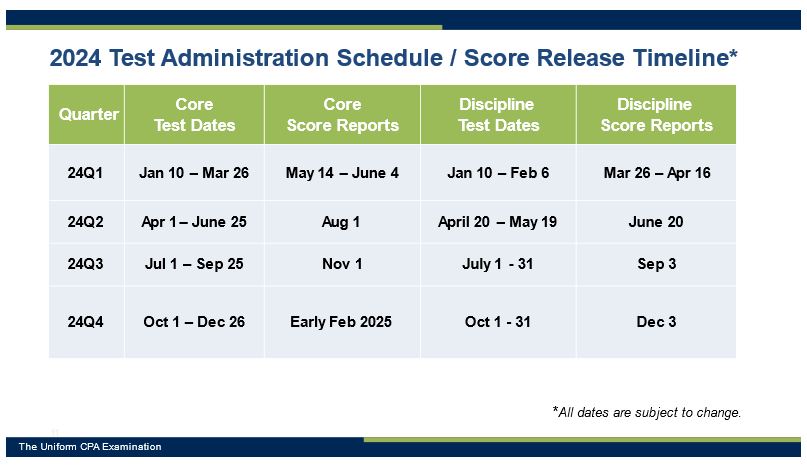

Q10 – Will a normal testing schedule be available for the 2024 CPA Exam sections? Will score releases follow historical patterns and be released every few weeks?

A10 – The tentative 2024 testing schedule and score release schedule is now available. Please note that these dates are tentative pending further review by AICPA. Both the testing schedules and the score release schedules will be atypical throughout 2024.

{kind=link}

It is currently anticipated that testing will commence on January 10, 2024, for all sections. While the Core sections (AUD, FAR and REG) will be available for scheduling through March 26, 2024, the Discipline sections (BAR, ISC and TCP) will only be available through February 6, 2024 in the first quarter. Scores are anticipated to only be released once per test section per quarter due to necessary standard-setting analyses and activities.

Q11 – Why is the CPA Exam schedule different for the Discipline Exam sections?

A11 – Candidates have a choice of which Discipline section to take, so not all candidates will take all Discipline sections. This means that for a given Discipline section, the number of candidates taking it will be much lower than the number of candidates taking the Core sections.

The analysis of test data requires a certain number of candidates. If a smaller number of candidates take an Exam section over a longer period, everyone will have to wait longer for scores. In order to minimize the amount of time any given candidate needs to wait for a score, the Discipline sections will be administered in a shorter period of time. The shorter time period for the Discipline sections also allows us to address other fairness and security objectives.

Q12 – Why will it take longer to get scores for the CPA Exam in 2024?

A12 – Whenever a new Exam is launched, additional analysis is needed to release candidate scores. The schedule for score releases in 2024 is similar to that in 2011 and 2017, when new versions of the CPA Exam were launched.

With the new Exam blueprints, there is a good deal of new content on the Exams, and this requires additional analysis after candidates have completed testing. For the first quarter of a new Exam, a new passing score must be set, and this requires further analysis in a number of steps. Accordingly, scores for the first quarter take longer than scores for subsequent quarters.

It is important to note that for each quarter in 2024, candidates will receive their scores in time to take the same Exam section in the next quarter if they choose.

Q13 – Should we expect that the 2024 testing schedule and score release schedule will be the new normal? Will testing be limited and score delays expected in 2025 and into the future?

A13 – We anticipate a more typical Exam schedule and score release timeline for the Core sections after 2024. Currently, we are unable to determine the Exam schedule and score release timeline for the Discipline sections post-2024.

Q14 – There are three new Core sections called AUD, FAR and REG. Does that mean they will remain the same as they are now?

A14 – Not exactly. The AUD Core section closely aligns with the current AUD section. Some content previously assessed in FAR, for example accounting for state and local governments, has been moved to the BAR Discipline. The REG Core section retains the same content areas, but some content currently assessed in REG has been allocated to the TCP Discipline. As part of the CPA Evolution initiative, the AICPA, under the governance of the Board of Examiners, has conducted a practice analysis research study, the results of which define the knowledge and skills required for each of the Core and Discipline sections of the 2024 CPA Exam. The 2024 CPA Exam Blueprints and test design were published in January 2023.

Q15 – Can I pass one of the new Discipline sections instead of passing AUD, FAR or REG?

A15 – No. Candidates will be required to pass AUD, FAR and REG under either the current Exam or the 2024 CPA Exam. Selecting and passing one Discipline section will replace passing BEC after the 2024 CPA Exam launches.

Q16 – Can I take more than one Discipline section of the Exam? If I pass one Discipline, may I take additional Disciplines?

A16 – No. Candidates are allowed to pass and retain credit for only one Discipline section starting in 2024, assuming they have not retained credit for BEC in 2023 or prior. Candidates may not take additional Disciplines. The only exceptions are (i) if a candidate’s credit for one Discipline expires or (ii) if a candidate fails a Discipline section, the candidate is allowed to select a different Discipline in which to be tested, if they so choose.

Q17 – Does the Discipline selected restrict future professional practice?

A17 – No. Regardless of chosen Discipline, this model leads to a full CPA license, with rights and privileges consistent with any other CPA. This includes rights to sign audit and attest reports, as the Core will give every candidate a strong base in accounting, auditing, tax and technology.

However, ethical requirements dictate that CPAs only undertake those professional services that they can reasonably expect to complete with professional competence. Competence means the CPA or their staff possess the appropriate technical qualifications to perform the professional service and that, as required, the CPA supervises and evaluates the quality of work performed.

Q18 – Should I be concerned that I won’t be able to find available Prometric appointments to schedule my CPA Exam section testing late in 2023?

A18 – Prometric understands that there could be high demand for CPA Exam testing appointments in the second half of 2023. As such, they are prepared to increase hours and add days, as possible. Candidates should not assume that appointments will be available exactly when and where they optimally wish to test. Candidates should schedule as early as possible and are strongly recommended to schedule at least 60 days or more in advance to obtain the best appointments available. Candidates are discouraged to wait until the last few days of a window to schedule appointments should there be weather or other events impacting testing.

Q19 – Will the way to schedule my appointment at Prometric change?

A19 – It will not change: you must continue to use the current Prometric online tools at CPA | Prometric should you need to check seat availability, locate sites, schedule, confirm or reschedule / cancel appointments.

Q20 – What should I know about the test day?

A20 – You can visit the Prepare For Test Day | Prometric page to know in advance what to expect at the test date. Also, you can watch the video on the What To Expect | Prometric page with important information on Prometric’s enhanced test center procedures you need to know for test day.

Q21 – How do I find out more about CPA Evolution and the 2024 CPA Exam structure and content?

A21 – Additional information is available at EvolutionofCPA.org, and any unanswered questions can be directed to [email protected]. Additionally, see the Practice Analysis Final Report and Uniform CPA Exam Blueprints that will be published in January 2023.