We use cookies to enhance the website experience and analyze performance and traffic on our website. Some cookies are essential to make our website work; others help us improve the user experience. Select "Accept All Cookies" to allow all uses of these cookies, "Decline Non-Essential Cookies" to limit cookies that are not required, and "Customize Cookies" for more options. You can update your cookie preferences at any time. Read our privacy policy to learn more.

PRESIDENT’S MEMO: “When E May Not Equal E”

SHARE:

It won’t be news to those in our NASBA family that the accounting profession has lately been grappling with an important question: What paths to becoming a CPA ensure both accessibility to the profession and competency within the profession?

These concepts—like “promotion of the profession” and “protection of the public”—can at times seem to stand on opposite sides. And yet we know that if the reputation of the CPA credential isn’t maintained through rigor, there won’t be much worth promoting about our profession. Similarly, the public won’t be as well protected if there are fewer and fewer protectors. As with many things in life, doesn’t it seem the best outcome depends on striking a balance between “opposed” views?

These days, though, it can seem balance itself—the compromises it demands—feels at risk. That increasingly we regard any dilution of our individual positions as either inviting danger or making us sellouts. But with any debate that’s complex in nature, it seems to me each side of it usually possesses a piece of the truth. When it comes to CPA pathways, you, our member boards—the regulators—have a vital piece of that truth. State societies do, too. Individual practitioners, academics, those at the start of their career and those near retirement from it—the same. NASBA, the AICPA, as well. Compromise among these views isn’t, therefore, a breaking from our truth but a joining of truths. And out of that compromise comes a correcting of our inevitable blind spots—NASBA’s included.

Recently, in order to educate myself, I did some digging in the NASBA archive. As it turns out, the debate surrounding education, experience, and the CPA has been around a while. Did you know that in the early days accountants were concerned about requiring too much education because the accounting programs within universities were not, in their view, good enough? This view morphed, however, after the profession noticed more people who graduated college passed the CPA Exam. Though they didn’t call it a pipeline issue then, accountants had grown to feel their discipline was increasingly multifaceted and that time spent in higher education would mean fewer people failing the Exam, thereby ensuring more CPAs. Indeed, in 1937—when there were only 39 State Boards of Accountancy—a controversial resolution emerged declaring that CPAs should have a college degree in accounting.

This resolution prompted a further discussion about what constituted proper experience: the years, the type, and whether that should be in private accounting versus public. A paper presented at a NASBA Regional Meeting in 1994 made the then-unconventional case that a liberal arts education was just as desirable for the unique skills it imparted to accountants. A response to this paper articulated the opposed belief that “learning through mistakes”—aka experience—was more vital. Which, interestingly, led to improvements in college programs that taught accounting. To the point that a new (well, old) consensus arose whose conclusion was that the best experience was indeed found in the classroom since other types of experience were susceptible to what was then criticized as “elapsed time”—that is: hours spent in an office by an accountant potentially doing little related to accountancy.

Back and forth we’ve gone. On education, experience, on education and experience—pieces of a more complete truth emerging at every pivot.

What I also found interesting in the archive was how, as these debates took place, the profession began to collaborate on a model of uniformity that could transcend divergent times, fashions of thought, and jurisdictional views. All so that accounting as a career balanced accessibility to the public with maintaining the trust the public put in it. In 1984, this work led to the joint Uniform Accountancy Act (UAA). Our profession has since been the envy of most, not just because those forward-thinking folks at the time created a model act that enhanced and preserved our unique mobility, but also because, as part of it, they devised a lesser-known process that works out our thorniest issues collectively. What that UAA process has addressed over four decades is impressive: transitioning the Exam from paper to computer, for example; peer review; CPA Evolution; and more.

Now, is this process—designed as it is to surface, explore and harmonize the views of a wide gamut of stakeholders—efficient? Not really. But then I’m beginning to wonder if we as a society haven’t become in thrall to a formula that, in many cases, is flawed. That being E=E, or “efficiency equaling excellence.” To name just one scenario, how many of us might swap efficiency in our medical appointments for a greater thoroughness that led to better care? Maybe the most vital matters in life are not meant to be efficient because they’re meant to be effective. And maybe it’s not speed but thoughtful completeness that brings human beings toward (ironically) time-saving truths and right action.

On pathways, there’s no question that NASBA and the AICPA should have been more efficient in taking the issue up. Many of you at the jurisdictional level already were and, for a number of reasons, we were late to your concerns. Which is why over the last two years, we’ve tried to make up for that oversight by mobilizing the UAA process. In establishing task forces, committees, and working groups that drew more than 60 individuals from state boards, state societies, firms, small practices, academia, NASBA, and the AICPA, we’ve worked together to find solutions. The result of this joint work was two draft proposals exposed for comment last September. If I may, I’d like to emphasize that word: proposal. We at NASBA never believed what these groups and the UAA Committee chose to expose was the end of the story, but rather a point of origin. One that would invite your expertise and thoughtful reactions to better shape an outcome.

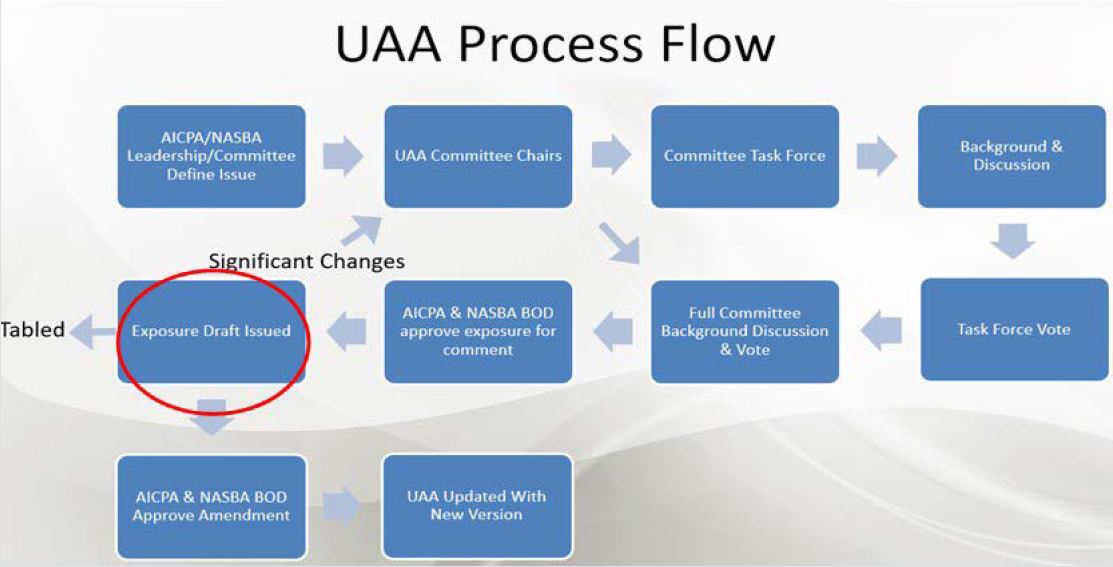

And shape it you have: Since the December deadlines, more than 500 comments on the proposals have been recorded. We are now sifting through the comments in order to join the truths of our stakeholders and overcome our blind spots. If you look at the flowchart graphic of the UAA process—included within this column—the comments and criticism you offered will result in either a tabled initiative or an entirely revised proposal to be exposed again. In this case, re-exposure is appropriate to align the UAA with the concepts contained in the exposure draft comments.

This isn’t a painless process. We are 55 U.S. jurisdictions, each with a position, an argument, often more than one. Part of NASBA’s promise to its members is not to shirk from, but catalyze, the most challenging yet essential debates facing our profession in order to help reconcile them. We should have moved quicker on the first part of that promise. But for the second part, the process itself, to proceed fast or autocratically—while that might seem “efficient” on the surface, it would neither honor our members nor be complete, truthful and ultimately effective.

Given our history, our professional nature as accountants, and this shared process, I am confident that we can and will find the right balance to this intricate and historic question.

Sincerely,

Daniel, J. Dustin

President and CEO