We use cookies to enhance the website experience and analyze performance and traffic on our website. Some cookies are essential to make our website work; others help us improve the user experience. Select "Accept All Cookies" to allow all uses of these cookies, "Decline Non-Essential Cookies" to limit cookies that are not required, and "Customize Cookies" for more options. You can update your cookie preferences at any time. Read our privacy policy to learn more.

What Are the Four CPA Exam Sections?

SHARE:

Author: Jenna Elkins, Communications and Digital Media Specialist

Posted: Dec. 8, 2020

One of the very first questions a CPA Exam candidate may ask is, “What are the four CPA Exam sections?” The Uniform CPA Examination (CPA Exam) is comprised of four sections, each four hours long: Auditing and Attestation (AUD), Business Environment and Concepts (BEC), Financial Accounting and Reporting (FAR) and Regulation (REG). It is critical for all candidates to know what to expect for each section in order to do well on the CPA Exam. To give a brief overview of each section, we have pulled information straight from the AICPA CPA Exam Blueprints.

Auditing and Attestation (AUD)

The AUD section of the CPA Exam tests the knowledge and skills that a newly licensed CPA must demonstrate when performing:

- Audits of issuer and nonissuer entities (including governmental entities, not-for-profit entities, employee benefit plans and entities receiving federal grants)

- Attestation engagements for issuer and nonissuer entities (including examinations, reviews and agreed-upon procedures engagements)

- Preparation, compilation and review engagements for nonissuer entities and reviews of interim financial information for issuer entities

Newly licensed CPAs are also required to demonstrate knowledge and skills related to professional responsibilities, including ethics, independence and professional skepticism. Professional skepticism reflects an iterative process that includes a questioning mind and a critical assessment of audit evidence. It is essential to the practice of public accounting and the work of newly licensed CPAs.

The following table summarizes the content areas and the allocation of content tested in the AUD section of the CPA Exam:

(graph from the AICPA CPA Exam Blueprints)

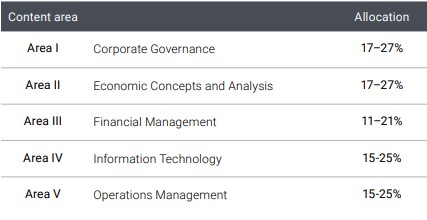

Business Environment and Concepts (BEC)

The BEC section of the CPA Exam tests knowledge and skills that a newly licensed CPA must demonstrate when performing:

- Audit, attest, accounting and review services

- Financial reporting

- Tax preparation

- Other professional responsibilities in their role as certified public accountants

The content areas tested under the BEC section of the CPA Exam encompass five diverse subject areas. These content areas are corporate governance, economic concepts and analysis, financial management, information technology and operations management.

(graph from the AICPA CPA Exam Blueprints)

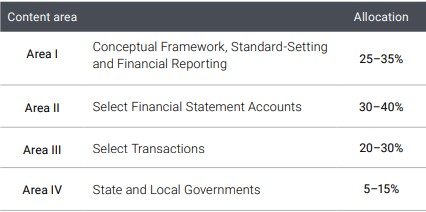

Financial Accounting and Reporting (FAR)

The FAR section of the CPA Exam assesses the knowledge and skills that a newly licensed CPA must demonstrate in the financial accounting and reporting frameworks used by business entities (public and nonpublic), not-for-profit entities and state and local government entities. The financial accounting and reporting frameworks that are eligible for assessment within the FAR section of the CPA Exam include the standards and regulations issued by the:

- Financial Accounting Standards Board (FASB)

- U.S. Securities and Exchange Commission (U.S. SEC)

- American Institute of Certified Public Accountants (AICPA)

- Governmental Accounting Standards Board (GASB)

- International Accounting Standards Board (IASB)

(graph from the AICPA CPA Exam Blueprints)

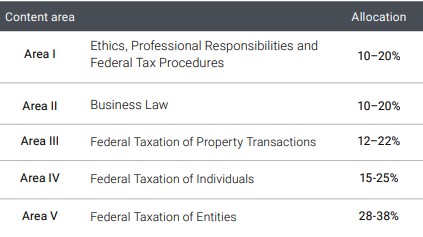

Regulation (REG)

The REG section of the CPA Exam tests the knowledge and skills that a newly licensed CPA must demonstrate with respect to:

- U.S. federal taxation

- U.S. ethics and professional responsibilities related to tax practice

- U.S. business law

(graph from the AICPA CPA Exam Blueprints)

Candidates who are looking for a more in-depth understanding of what information is on the CPA Exam, a review of the CPA Exam Blueprints is a must. This document is published one to two times per year and details the minimum level of knowledge and skills candidates must have to qualify for licensure.

To understand the CPA Exam journey as a whole, the Candidate Guide is a great place to start. Best of luck to all candidates who are on they way to becoming a Certified Public Accountant!