Enforcement NewsletterJanuary 2017

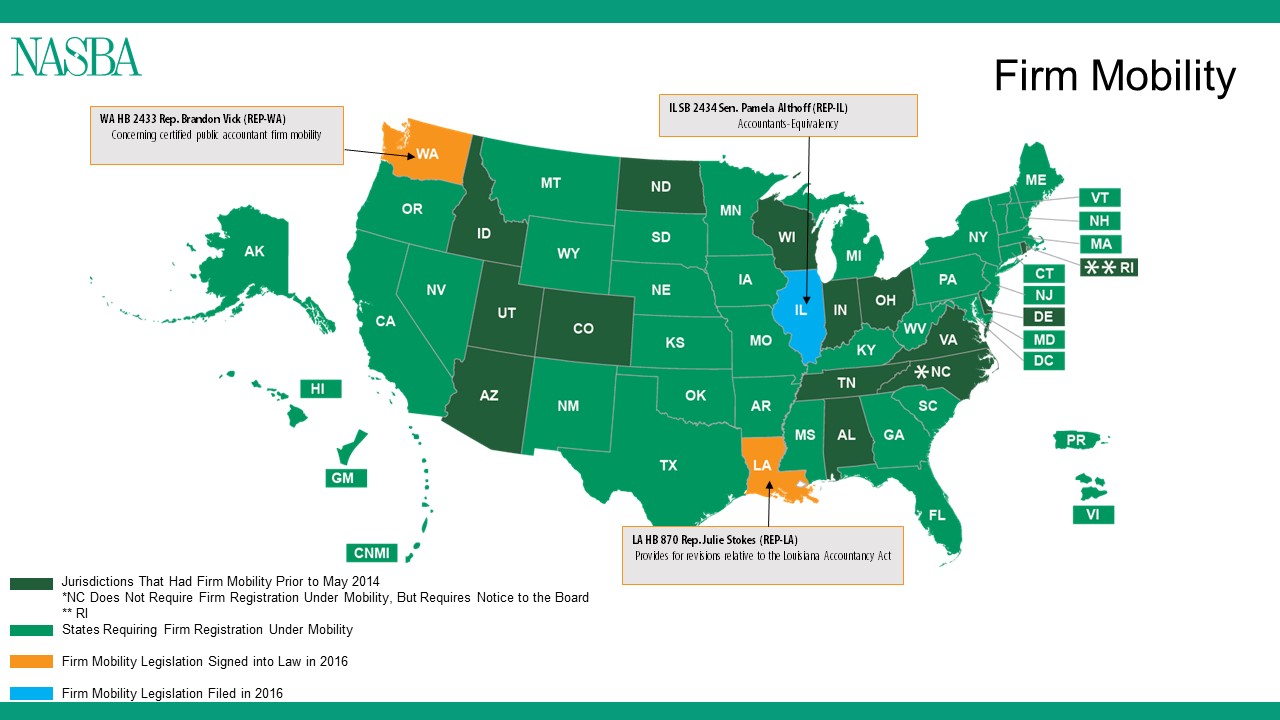

The Seventh Edition of the Uniform Accountancy Act (UAA) was tweaked in May 2014 to include Firm Mobility. In short, Firm Mobility allows a CPA firm to provide attest services in another state where it is not registered and does not have a physical office, under a “no notice, no fee, no escape” regime. The new language builds off the UAA’s concepts regarding individual CPA mobility, which have been adopted in 52 of the 55 U.S. jurisdictions. Prior to Firm Mobility being added to the UAA, there were 14 jurisdiction that had already adopted the principle. Since then, there have only been three jurisdictions that have filed firm mobility legislation – all in 2016. Of the three bills filed, two of those have been signed into law – in the states of Washington and Louisiana. For more information about Firm Mobility, contact John Johnson, NASBA’s Director of Legislative and Governmental Affairs, at [email protected] or 615.880.4232. |